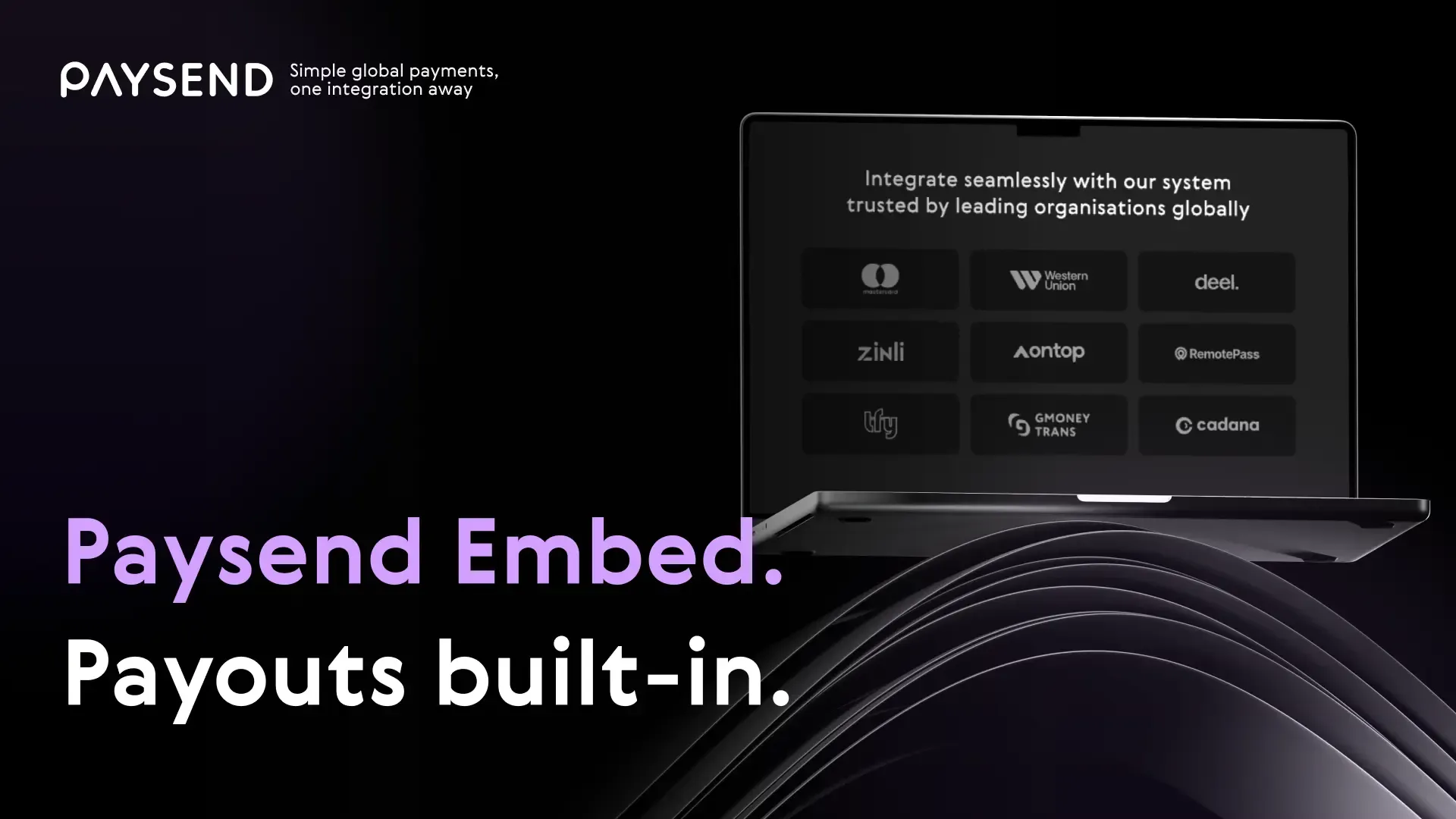

Paysend Embed: the widget powering seamless cross-border payouts

Behind every smooth international transaction is powerful infrastructure. With Paysend Embed, licensed institutions, fintechs, and digital platforms can integrate instant, compliant payouts into their apps, bringing their users closer to a truly borderless experience.

As part of Paysend’s mission to build the world’s largest digital payment network, Embed helps partners break barriers in cross-border money movement. It’s designed for teams that want to stay in control of their user experience, while Paysend powers the secure, compliant movement of funds behind the scenes.

Built for licensed institutions

For banks, regulated financial institutions, and licensed entities, Embed offers a white-label-ready widget that fits seamlessly into existing digital ecosystems. You maintain full control of your customer experience while Paysend handles global delivery, compliance, and infrastructure.

Key features:

- Native widget for app and web integration

- Tier 1 licensing and infrastructure

- Fast go-to-market

- Enterprise-level scalability

Built for fintechs

For startups and scaleups ready to expand across borders, Embed accelerates growth. With one integration, fintechs can embed international payouts directly into their products, unlocking new functionality, new markets, and new revenue streams in days, not months.

Key features:

- Fully embeddable widget

- Access to 100+ global corridors

- Licensed and compliant rails

- Rapid deployment

Built for the creator and gig economy

Modern platforms are global by default, and their users expect to get paid the same way. Embed empowers gig and creator platforms to deliver real-time* payouts inside their own ecosystems, giving freelancers, creators, and contractors faster access to their earnings.

Key features:

- Multi-currency, multi-market support

- Mobile-first widget integration

- Real-time payouts to card, wallet, or bank

- Scalable for high-volume businesses

Breaking barriers in global payouts

Paysend Embed addresses the biggest pain points in cross-border money transfer – compliance, licensing, and infrastructure – so partners can focus on innovation. It’s part of our mission to bring simple, secure money transfer to all, including the underserved, while giving businesses the tools to scale globally with confidence.

*Please note: Your money will be sent in real time; however, transfer delivery times may vary based on recipient bank processing, compliance checks, or other factors.

Latest Posts

Sending money digitally is quick and convenient, but it also involves important security, verification, and fraud prevention checks. In most cases these checks happen automatically in the background.

If you’ve ever wondered why Paysend asks you to verify your identity, why a transfer might be reviewed, or how your money is protected, the answer is simple: these processes are designed to keep you, your money, and your recipient safe.

Every digital money transfer relies on trust, regulation, and security systems working together. While these checks can sometimes feel like an extra step, they are a standard and essential part of how modern money transfers stay secure.

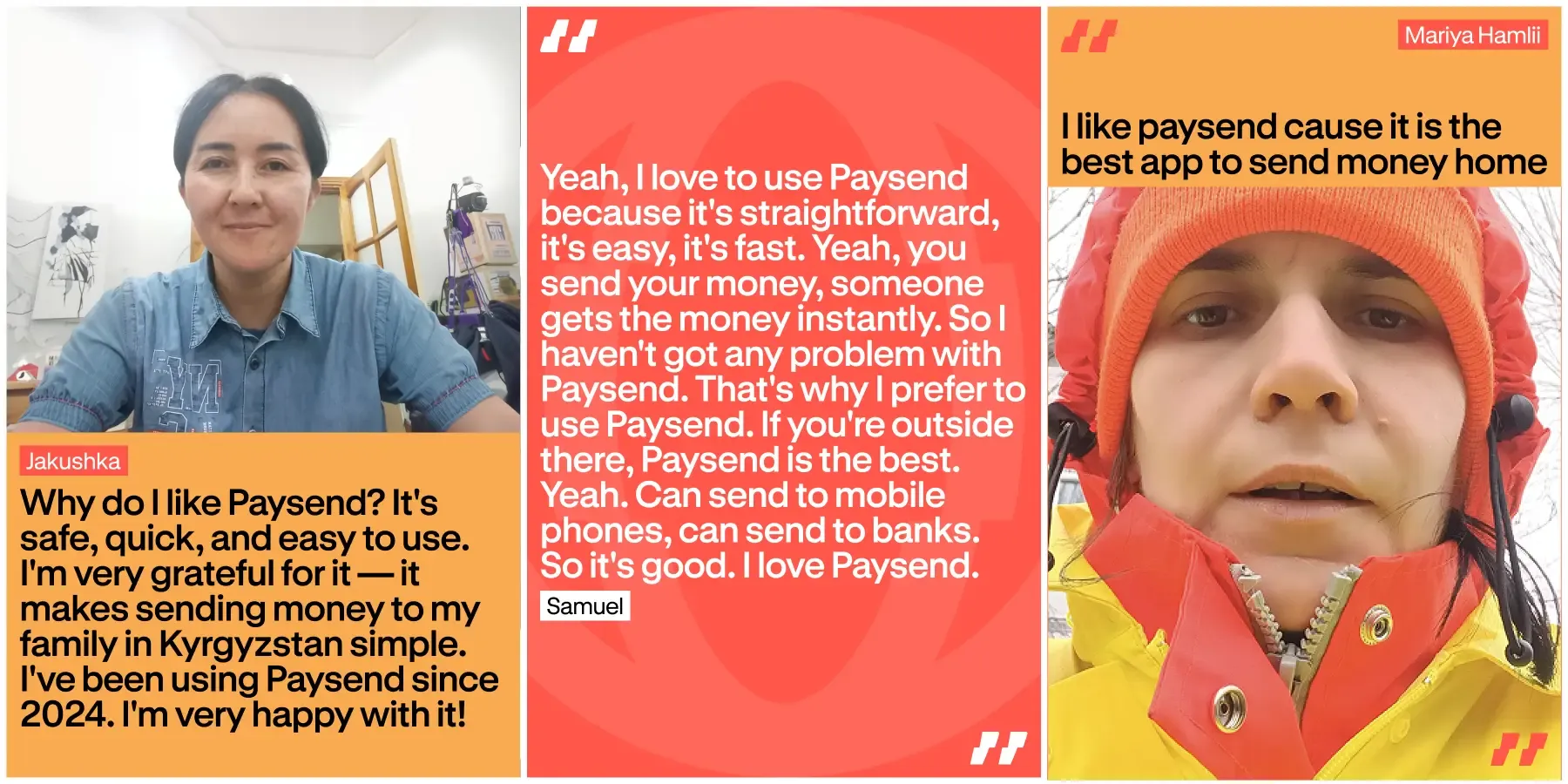

Sending money abroad should feel easy and safe. With Paysend, people know their money will arrive quickly and without stress. It’s not just about speed – it’s about trust, security, and knowing it works every time.

This article shares real customer experiences and why reliability matters in everyday life. It shows how people describe Paysend, and how the network helps move money safely across the world, every day.