Inside the India & Nepal Corridors: What Our Users Are Telling Us - By Paysend’s South Asia Regional Lead

Few regions illustrate the power of remittances better than India and Nepal.

In India and Nepal corridors, remittances are not a discretionary financial activity — they are part of daily life. What we see consistently is that users arrive with high intent and very little patience for friction. It's critical to have a fast, clear, and trustworthy user experience.

And over the past year, we’ve seen clear patterns emerge from our growing user base.

What We’re Seeing on the Ground

First, usage is rising. Paysend is experiencing strong growth in monthly active users across India and Nepal — a sign that people are actively choosing digital, app-based transfers over slower or more expensive alternatives.

Second, seasonality matters:

- Transfers spike around school terms, festivals, and major holidays

- There’s consistent demand at the start of the year, when families plan budgets and expenses

- Speed becomes especially critical during festivals and emergencies

Third, mobile-first behaviour is the norm. Users expect transfers to work instantly, clearly, and without the need for branches or paperwork. If it’s not simple, they move on.

Why Paysend Fits These Corridors

What’s driving adoption isn’t just cost — it’s confidence:

- Confidence that money will arrive quickly

- Confidence in transparent exchange rates

- Confidence that the app will work when it’s most needed

For families in India and Nepal, remittances are about stability. Paysend’s role is to support that stability — quietly, reliably, and at scale.

Looking Ahead

As these corridors continue to grow, our focus remains the same: listen closely to user behaviour, remove friction where it matters most, and build experiences that people trust with something deeply personal — supporting their families.

And for those sending regularly, we make sure to give back — with offers, promotions, and giveaways throughout the year.

Follow @Paysend on Instagram to stay in the loop.

Because behind every transfer is a family — and that’s what drives everything we do.

The educational materials on this site are provided for informational purposes only and do not reflect the opinions of Central Bank of Kansas City, Member FDIC. Educational materials may contain links to content on third-party websites which are provided for your convenience; please note that linked sites may have a privacy and security policy different from our own, and we cannot attest to the accuracy of information. The Central Bank of Kansas City does not guarantee nor expressly endorse any particular business, product, service, or third-party content.

Latest Posts

Sending money digitally is quick and convenient, but it also involves important security, verification, and fraud prevention checks. In most cases these checks happen automatically in the background.

If you’ve ever wondered why Paysend asks you to verify your identity, why a transfer might be reviewed, or how your money is protected, the answer is simple: these processes are designed to keep you, your money, and your recipient safe.

Every digital money transfer relies on trust, regulation, and security systems working together. While these checks can sometimes feel like an extra step, they are a standard and essential part of how modern money transfers stay secure.

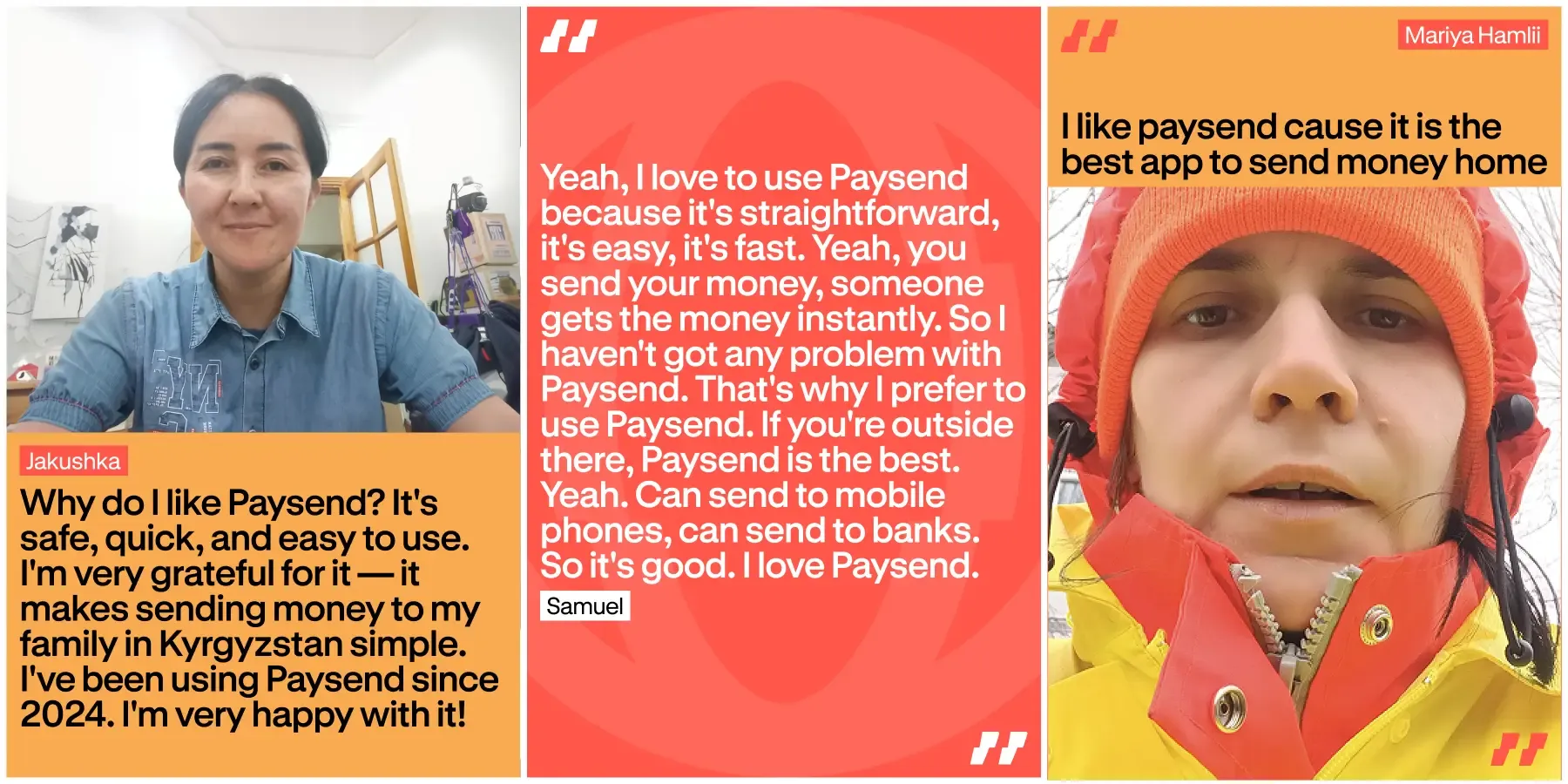

Sending money abroad should feel easy and safe. With Paysend, people know their money will arrive quickly and without stress. It’s not just about speed – it’s about trust, security, and knowing it works every time.

This article shares real customer experiences and why reliability matters in everyday life. It shows how people describe Paysend, and how the network helps move money safely across the world, every day.