How to redeem a Paysend promo code: a step-by-step guide

Looking for a little extra bonus when sending money abroad? Promo codes are a great way to save more or receive additional benefits on your international money transfers. Whether it’s during a special promotion or sent to you as a treat, claiming your Paysend bonus code is simple.

Here’s everything you need to know about using promo codes, from where to find them to how to apply them, so you can make the most of your international transfers.

How to use a Paysend promo code

Follow these easy steps to claim your bonus:

1. Select recipient

2. Select how to deliver money to recipient

- Enter recipient’s details

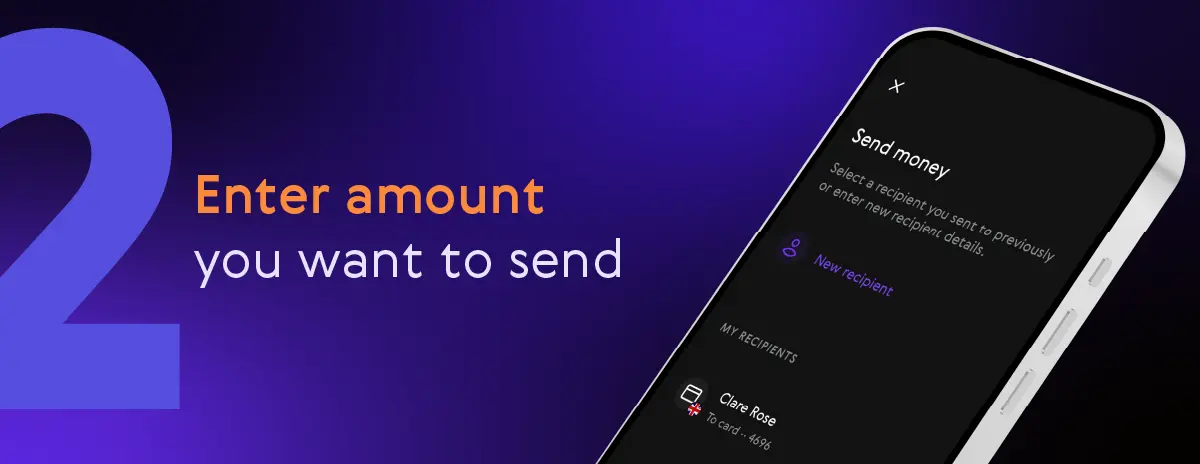

- Enter amount you want to send

3. Select Add a code

4. Enter promo code

5. Select your payment method

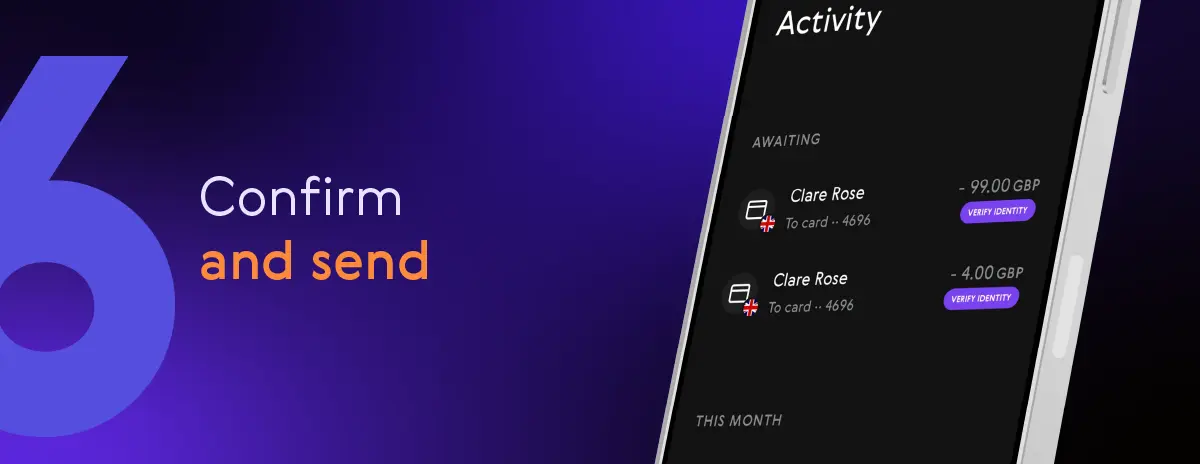

6. Confirm and send

If it’s a fee-free Promo Code your zero fee will be applied automatically. If it’s a Bonus Promo Code, you’ll receive the bonus directly to your Paysend account once the transfer has been completed and the recipient has received their money.

Common questions about promo codes

How can I get a Paysend promo code?

At Paysend we occasionally share promo codes through our official communication channels, such as email and push notifications. These codes are sometimes sent at special times and celebrations to reward our much-valued customers and make your money transfers go further.

If you’re looking for a promo code online, be cautious - promo codes shared by third parties or social media comments may not be valid or available for everyone. If you’re eligible for a promo code, you’ll receive it directly from Paysend.

Can I use promo codes at any time?

Promo codes are typically valid for a limited period, so it’s essential to check your email or push notification for the expiry date. Make sure to use your code before it runs out, so you don’t miss the opportunity to enjoy the bonus!

What if my promo code doesn’t work?

If your promo code isn’t working, here are some common reasons and fixes:

- Incorrect entry: Promo codes are case-sensitive. Double-check that you’ve typed the code exactly as it appears in your email or push notification.

- Expired code: Ensure the code is still valid by checking the expiry date.

- Eligibility: Some promo codes are specific to certain users or regions. If you didn’t receive the code directly from Paysend, it might not be valid for your account.

If your promo code hasn’t expired but still doesn’t work, don’t worry. Our customer service team is here to help. Contact us through the Help Centre or the in-app support feature. They’ll investigate the issue and ensure you’re able to claim your bonus.

Enter your promo code carefully

When using a promo code, accuracy matters. Be sure to type the code exactly as it’s shown, including capitalisation. If you see an “Incorrect code” message, double-check your input and try again.

Ready to claim your bonus?

Don’t wait - promo codes are a limited-time treat! Follow the steps above to send money quickly, securely, and with a little extra in your pocket. If you’ve received a Paysend promo code, take advantage of it today and make your international transfers even more rewarding.

Publikasi Terbaru

Sending money digitally is quick and convenient, but it also involves important security, verification, and fraud prevention checks. In most cases these checks happen automatically in the background.

If you’ve ever wondered why Paysend asks you to verify your identity, why a transfer might be reviewed, or how your money is protected, the answer is simple: these processes are designed to keep you, your money, and your recipient safe.

Every digital money transfer relies on trust, regulation, and security systems working together. While these checks can sometimes feel like an extra step, they are a standard and essential part of how modern money transfers stay secure.

Sending money abroad should feel simple, but if your international transfer is delayed or not received, it’s natural to wonder what went wrong.

International money transfers can be delayed, held, or returned for several reasons, most commonly due to compliance checks, missing information, processing cut-off times, or intermediary bank reviews. Industry reporting suggests that while the majority of transfers complete successfully, a small but meaningful share requires manual handling or additional processing, which can cause delays.

It’s important to understand that international money transfers involve multiple institutions, compliance checks, and settlement systems. Because of this, delays or exceptions are not unusual and are typically linked to process or regulatory requirements rather than technical failures or user mistakes.

With that in mind, this guide explains why international transfers may not be received as expected, how often this happens and what you can realistically do next.