Geleceği düşünüyoruz.

En son Paysend makalelerini okuyun

Throughout August, Paysend is doubling referral rewards. Invite a friend and you'll earn $6 USD, or equivalent local currency, for every successful referral — up to $72 in total. The offer runs from 1 to 31 August, and it applies automatically to every eligible referral made during that window.

Referring friends to Paysend already earns a reward in a normal month. This August, that reward simply goes further. Every friend who joins through your link and completes a qualifying transfer earns you $6 instead of the usual $3, and the total you can earn across the month rises from $36 to $72. It’s easy to invite a friend - just share your invite a friend link found in the app.

Sending money digitally is quick and convenient, but it also involves important security, verification, and fraud prevention checks. In most cases these checks happen automatically in the background.

If you’ve ever wondered why Paysend asks you to verify your identity, why a transfer might be reviewed, or how your money is protected, the answer is simple: these processes are designed to keep you, your money, and your recipient safe.

Every digital money transfer relies on trust, regulation, and security systems working together. While these checks can sometimes feel like an extra step, they are a standard and essential part of how modern money transfers stay secure.

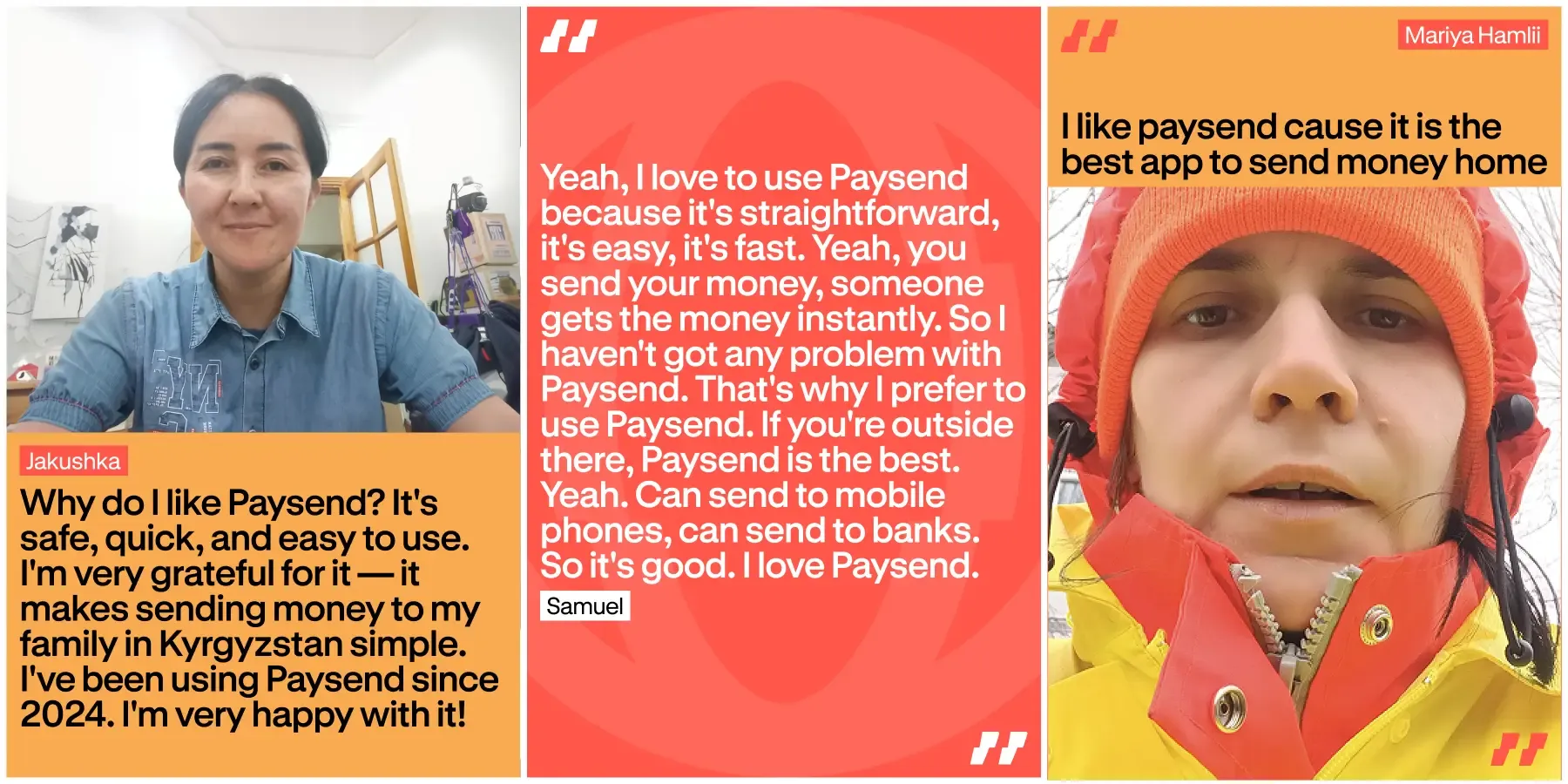

Yurt dışına para göndermek kolay ve güvenli hissettirmelidir. Paysend ile insanlar paralarının hızlı ve sorunsuz bir şekilde ulaşacağını bilir. Bu sadece hızla ilgili değil – güven, güvenlik ve her seferinde sorunsuz çalıştığını bilmekle ilgilidir.

Bu makale, gerçek müşteri deneyimlerini ve güvenilirliğin günlük hayatta neden önemli olduğunu paylaşıyor. İnsanların Paysend’i nasıl tanımladığını ve ağın parayı her gün dünya genelinde nasıl güvenle taşıdığını gösteriyor.

Sending money abroad should feel simple, but if your international transfer is delayed or not received, it’s natural to wonder what went wrong.

International money transfers can be delayed, held, or returned for several reasons, most commonly due to compliance checks, missing information, processing cut-off times, or intermediary bank reviews. Industry reporting suggests that while the majority of transfers complete successfully, a small but meaningful share requires manual handling or additional processing, which can cause delays.

It’s important to understand that international money transfers involve multiple institutions, compliance checks, and settlement systems. Because of this, delays or exceptions are not unusual and are typically linked to process or regulatory requirements rather than technical failures or user mistakes.

With that in mind, this guide explains why international transfers may not be received as expected, how often this happens and what you can realistically do next.