From Pigeons to Paysend: A Brief History of Sending Money Home

Long before apps, banks, or even paper money, people still had the same need we have today:

to send value across distance.

What’s changed isn’t the motivation — it’s the method.

The Earliest Transfers: Trust and Ingenuity

Centuries ago, money didn’t move digitally — it moved through people, animals, and reputation.

Merchants relied on trusted couriers. Messages and instructions were carried across borders by foot, horse… and yes, even pigeons. Value was transferred not through systems, but through relationships.

It was slow. It was risky. But it worked — because it had to.

The Rise of Informal Networks

As trade expanded, informal systems like hawala emerged. These networks allowed money to move quickly without physically crossing borders, based entirely on trust and local agents.

For many communities, this was revolutionary. Funds could move fast, even where banks didn’t exist.

But informality came at a cost:

- No guarantees

- No transparency

- No protection if something went wrong

Trust lived in people — not in systems.

Banks, Wires, and the Age of Institutions

The 20th century brought formal banking, wire transfers, and global financial institutions. Money became more secure — but also more complicated.

Sending money internationally often meant:

- Visiting a branch

- Filling out forms

- Waiting days for confirmation

- Paying unclear fees

For decades, this was the only “safe” option — even if it wasn’t convenient.

Digital Disruption: When Money Finally Caught Up

Then came the smartphone.

Suddenly, people expected money to move the way messages do —fast, clearly, and from anywhere. Digital remittance platforms began replacing paper forms and long queues with apps and real-time notifications.

This shift wasn’t about novelty. It was about meeting real human needs:

- Urgent support

- Predictable timing

- Transparent costs

From Pigeons to Paysend

Paysend represents the latest chapter in a very old story.

Like the earliest couriers, Paysend is about connection.

Like informal networks, it prioritizes speed.

Like modern banking, it delivers security and compliance.

But unlike anything before it, Paysend brings all of this together — in one simple, mobile-first experience.

Today, sending money home no longer requires waiting, guessing, or hoping for the best. It happens in minutes, with clarity and confidence. Your money will be sent in real time; however, transfer delivery times may vary based on recipient bank processing, compliance checks, or other factors

The Constant Through History

Across centuries and technologies, one thing has never changed:

People send money because they care.

From pigeons to Paysend, the tools may evolve — but the purpose stays the same.

And in 2026, that purpose deserves a solution built for modern life.

With Paysend, you’re not just using the latest technology — you’re part of a long human tradition, made simpler, faster, and more reliable than ever before.

The materials on this blog are provided for informational purposes only and do not reflect the opinions of Central Bank of Kansas City, Member FDIC. Blog posts may contain links to content on third-party websites, which are provided for your convenience; please note that linked sites may have a privacy and security policy different from our own, and we cannot attest to the accuracy of information. The Central Bank of Kansas City does not guarantee nor expressly endorse any particular business, product, service, or third-party content.

Останні дописи

Sending money digitally is quick and convenient, but it also involves important security, verification, and fraud prevention checks. In most cases these checks happen automatically in the background.

If you’ve ever wondered why Paysend asks you to verify your identity, why a transfer might be reviewed, or how your money is protected, the answer is simple: these processes are designed to keep you, your money, and your recipient safe.

Every digital money transfer relies on trust, regulation, and security systems working together. While these checks can sometimes feel like an extra step, they are a standard and essential part of how modern money transfers stay secure.

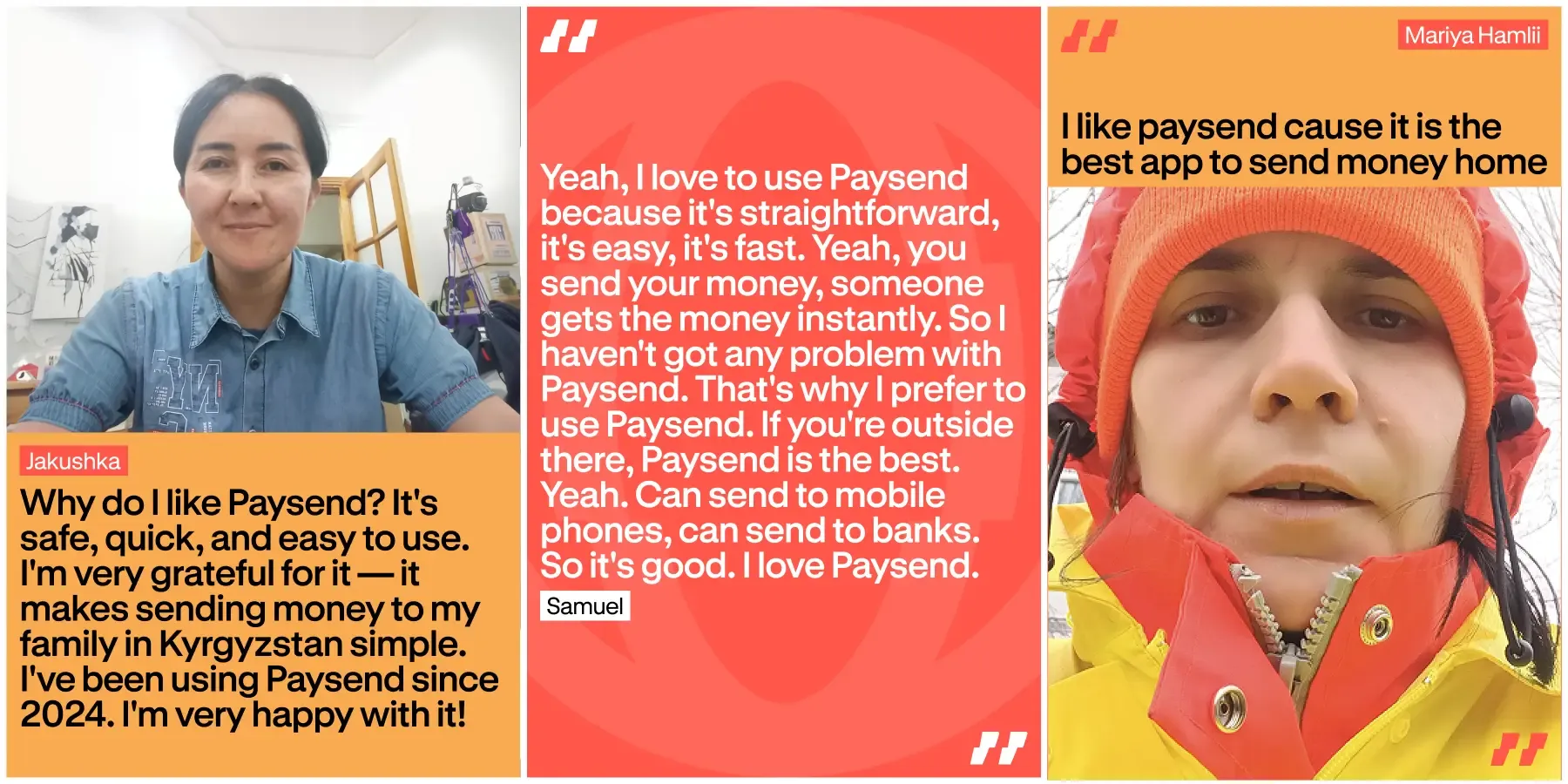

Надсилання грошей за кордон має бути простим і безпечним. З Paysend люди знають, що їхні гроші надійдуть швидко і без зайвого стресу. Справа не лише у швидкості – йдеться про довіру, безпеку та впевненість у тому, що сервіс працює щоразу.

У цій статті ми ділимося реальними відгуками клієнтів і пояснюємо, чому надійність важлива у повсякденному житті. Тут показано, як люди описують Paysend і як мережа допомагає безпечно переказувати гроші по всьому світу щодня.