The digital evolution compared to traditional money transfers

Not long ago, sending money abroad meant standing in line, filling out forms, and hoping your recipient could collect the cash before the office closed. For decades, this may have been the reality of traditional money transfers: long waits, limited hours, and high fees.

Today, digital-first services like Paysend may have changed that story completely. Money now moves in real-time*, anytime and around the world. This evolution isn’t just about technology; it’s about breaking barriers and addressing the main pain points in cross-border money transfer.

*We’ll send your money in real-time, but it could take up to 3 business days depending on your recipient’s bank processing time.

What are traditional (agent-based) transfers?

Traditional or agent-based money transfers may rely on physical locations and cash transactions. Companies like Western Union and MoneyGram built large global networks that allow senders to deliver money in person and recipients to collect it in cash.

How it works:

- The sender visits a physical agent location.

- They complete forms, hand over cash, and pay a service fee.

- The recipient goes to another agent to collect the funds in cash.

The pain points:

- Limited business hours and may have long lines.

- May involve higher costs and slower processing due to cash handling and network overheads.

- May experience delays in delivery and may have limited fee visibility.

- May be inconvenient for senders and recipients who rely on speed and flexibility. All comparative statements are based on publicly available information as of Nov 2025. Western Union and MoneyGram are trademarks of their respective owners. This article is intended for informational purposes only and does not constitute an endorsement or partnership.

This model served its purpose for many years, but as the world became more connected, people demanded something faster, simpler, and more transparent.

The rise of digital-first transfers

Digital-first platforms like Wise, Remitly, WorldRemit, and Paysend transformed the international money transfer experience. Instead of visiting an agent, users can send funds directly from an app or website, often in minutes.

As highlighted by Fintech Global, Paysend actually pioneered the concept of card-to-card money transfers, enabling users to send funds directly between debit or credit cards across major payment networks such as Visa, Mastercard, and UnionPay. Unlike traditional bank transfers that may required complex details such as IBANs and SWIFT codes, Paysend simplified the process by allowing customers to transfer money using just the recipient’s name and their card’s 16-digit number. This innovation eliminated paperwork, sped up transactions, and provided transparency with competitive exchange rates and flat, low fees, making global money transfers fast, and more accessible. By connecting billions of cards in over 100 countries, Paysend set a new industry standard for convenience, security, and efficiency in cross-border payments.

What makes digital-first transfers different:

- Online onboarding with secure verification.

- Real-time exchange rates and transparent fees.

- Real-time* transfers to cards, bank accounts, and wallets.

- 24/7 availability through mobile and web platforms.

These platforms have built trust by putting customers first — offering clarity, convenience, and control at every step.

*We’ll send your money in real-time, but it could take up to 3 business days depending on your recipient’s bank processing time.

Why digital evolution matters

The move from traditional to digital money transfer isn’t just about speed. It’s about giving people more power over their finances.

Digital transfers mean:

- Transparency – clear pricing and guaranteed exchange rates.

- Speed – fast delivery

- Security – encrypted transactions, regulated systems, and PCI DSS compliance.

- Accessibility – 24/7 access from your phone, no need to visit a physical location.

This digital evolution may have made international money transfers fairer, faster, and more inclusive – supporting millions of people who depend on remittances worldwide.

All trademarks, service marks, and trade names referred to in this material

are the property of their respective owners.

Paysend and the power of digital innovation

Paysend is on a mission to bring simple money transfer to all, including the underserved. Through our technology, users can send money directly from card to card in seconds* — a global innovation that eliminates middlemen and delays.

With Paysend, you can:

- Send to over 100 countries through one app or website.

- Enjoy a flat, transparent fee with no surprises.

- Access real-time exchange rates and fast delivery.

- Move money securely across borders anytime, anywhere.

We’re building the world’s largest digital payment network — helping people stay connected across borders while addressing the core pain points of traditional money transfers.

*We’ll send your money in real-time, but it could take up to 3 business days depending on your recipient’s bank processing time.

Why traditional transfers still exist and where digital wins

Traditional cash pickups still matter in markets where digital access is limited or unbanked populations rely on physical cash. But the global trend is clear — more people are turning to digital remittances every year.

Where digital wins:

- Greater smartphone adoption and internet access.

- Seamless app-based experiences.

- Instant notifications and tracking.

- May have lower transfer costs and more transparency.

Digital remittances are not just the future, they are already the present for millions of people sending money overseas.

The future is in your pocket

While traditional agent networks continue to serve customers who rely on cash, the global trend increasingly favors digital solutions. Digital-first platforms like Paysend are making international money transfer fast, fair, and accessible for all.

Paysend’s vision remains to build the world’s largest digital payment network, and in the process the company is breaking barriers and redefining what global connection looks like – helping families, freelancers, and businesses move money safely and fast, wherever they are.

Send money abroad fast, securely, and without hidden fees, all from your phone.

The educational materials on this site are provided for informational purposes only and do not reflect the opinions of Central Bank of Kansas City, Member FDIC. Educational materials may contain links to content on third-party websites which are provided for your convenience; please note that linked sites may have a privacy and security policy different from our own, and we cannot attest to the accuracy of information. The Central Bank of Kansas City does not guarantee nor expressly endorse any particular business, product, service, or third-party content.

Disclaimer: All comparative statements are based on publicly available information as of Nov 2025. Western Union and MoneyGram are trademarks of their respective owners. This article is intended for informational purposes only and does not constitute an endorsement or partnership.

Latest Posts

Sending money digitally is quick and convenient, but it also involves important security, verification, and fraud prevention checks. In most cases these checks happen automatically in the background.

If you’ve ever wondered why Paysend asks you to verify your identity, why a transfer might be reviewed, or how your money is protected, the answer is simple: these processes are designed to keep you, your money, and your recipient safe.

Every digital money transfer relies on trust, regulation, and security systems working together. While these checks can sometimes feel like an extra step, they are a standard and essential part of how modern money transfers stay secure.

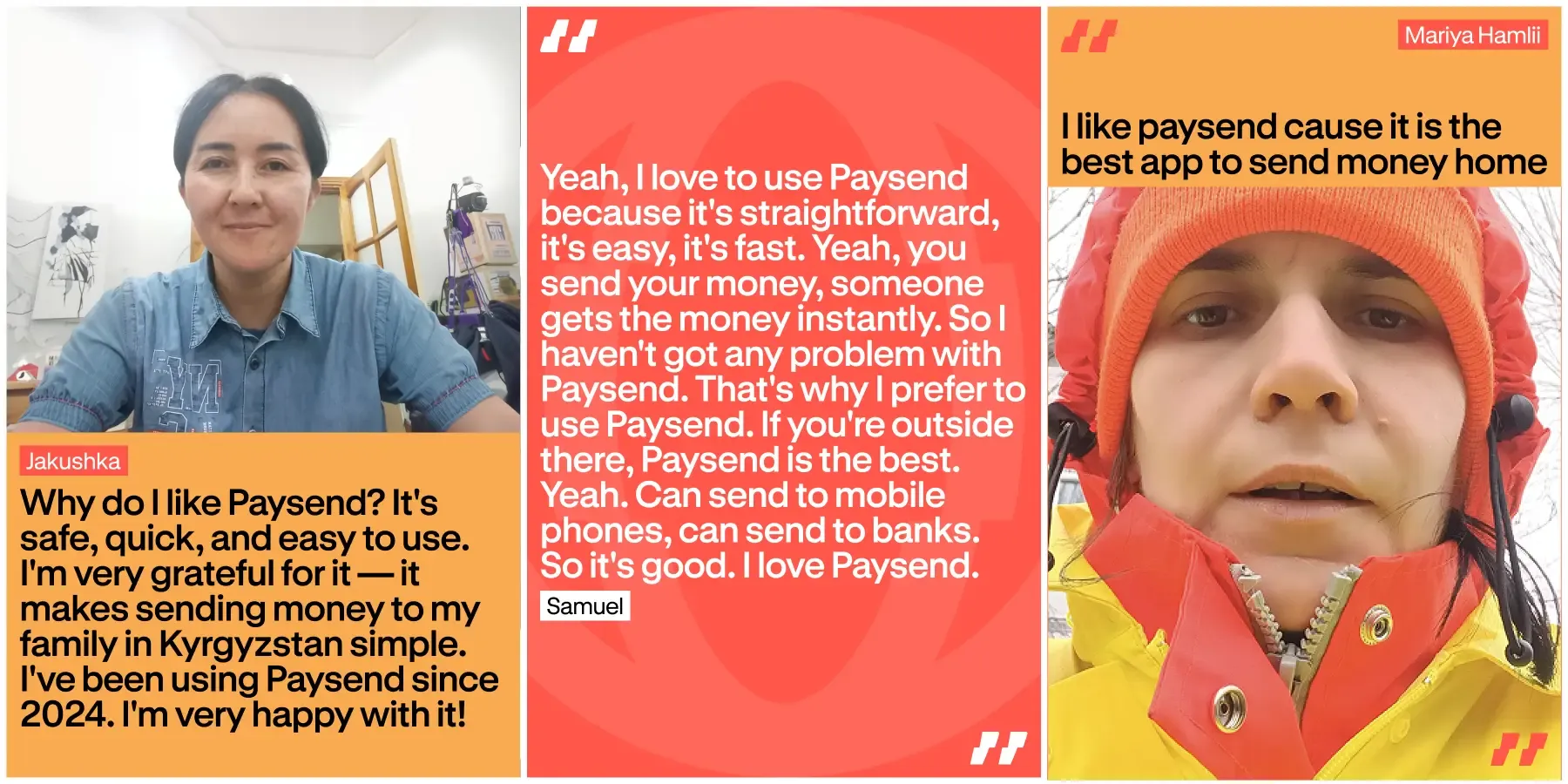

Sending money abroad should feel easy and safe. With Paysend, people know their money will arrive quickly and without stress. It’s not just about speed – it’s about trust, security, and knowing it works every time.

This article shares real customer experiences and why reliability matters in everyday life. It shows how people describe Paysend, and how the network helps move money safely across the world, every day.