Pensando en el futuro.

Lee los últimos artículos de Paysend

Sending money digitally is quick and convenient, but it also involves important security, verification, and fraud prevention checks. In most cases these checks happen automatically in the background.

If you’ve ever wondered why Paysend asks you to verify your identity, why a transfer might be reviewed, or how your money is protected, the answer is simple: these processes are designed to keep you, your money, and your recipient safe.

Every digital money transfer relies on trust, regulation, and security systems working together. While these checks can sometimes feel like an extra step, they are a standard and essential part of how modern money transfers stay secure.

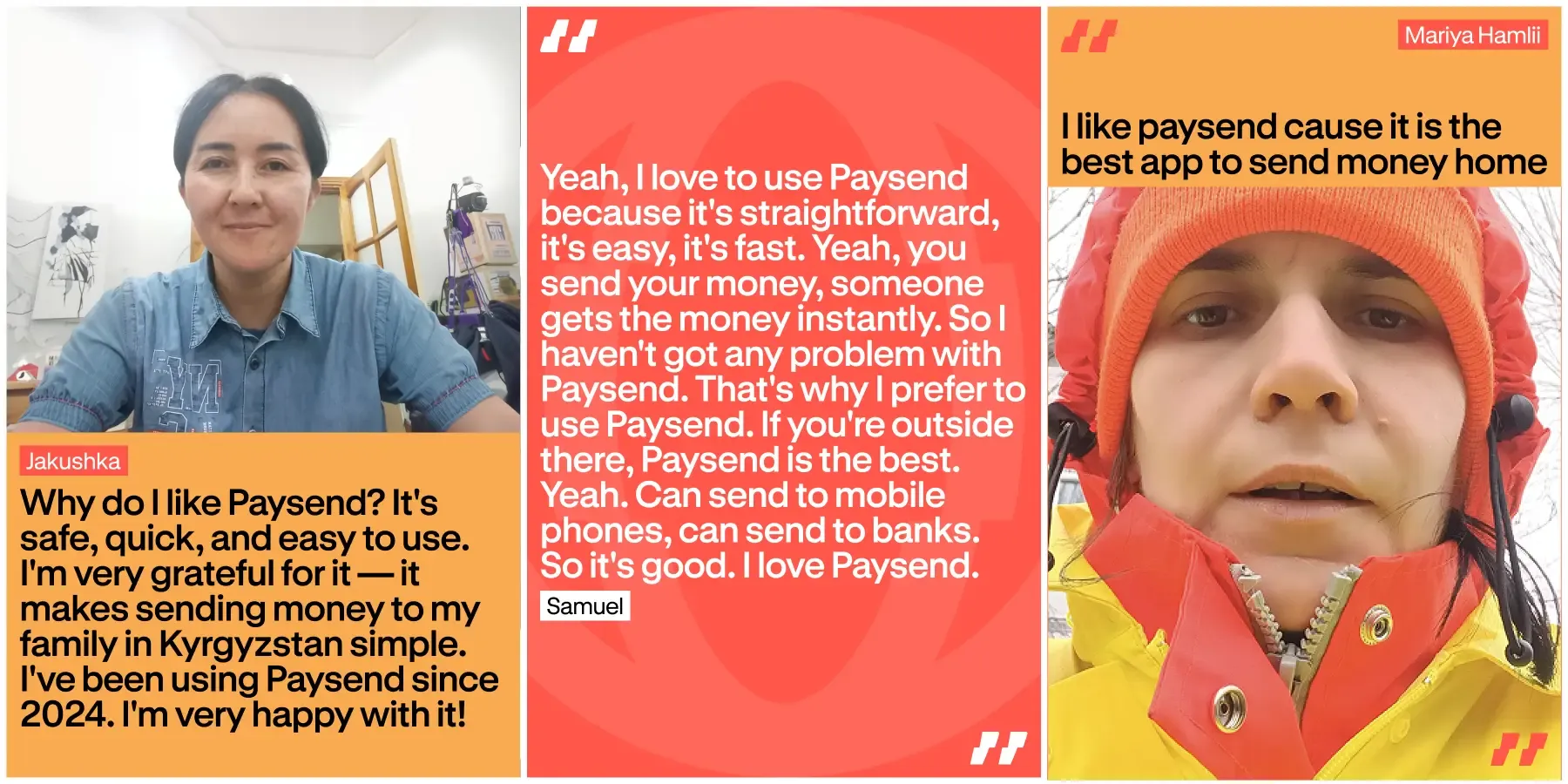

Enviar dinero al extranjero debe sentirse fácil y seguro. Con Paysend, las personas saben que su dinero llegará rápido y sin estrés. No se trata solo de velocidad – se trata de confianza, seguridad y saber que funciona cada vez.

Este artículo comparte experiencias reales de clientes y explica por qué la confiabilidad importa en la vida cotidiana. Muestra cómo las personas describen Paysend y cómo la red ayuda a mover dinero de forma segura por todo el mundo, todos los días.

Sending money abroad should feel simple, but if your international transfer is delayed or not received, it’s natural to wonder what went wrong.

International money transfers can be delayed, held, or returned for several reasons, most commonly due to compliance checks, missing information, processing cut-off times, or intermediary bank reviews. Industry reporting suggests that while the majority of transfers complete successfully, a small but meaningful share requires manual handling or additional processing, which can cause delays.

It’s important to understand that international money transfers involve multiple institutions, compliance checks, and settlement systems. Because of this, delays or exceptions are not unusual and are typically linked to process or regulatory requirements rather than technical failures or user mistakes.

With that in mind, this guide explains why international transfers may not be received as expected, how often this happens and what you can realistically do next.

You can send money to Bulgaria directly to a Visa card or bank account with Paysend — an international money transfer service covering more than 170 countries. Transfers use a fixed-fee pricing model, with funds arriving fast. Your money travels a trusted global route, safe, fair, and on time.